Indirect Security

Indirect security refers to a type of collateral provided for a loan.

What is Indirect Security?

Indirect security refers to a type of collateral provided for a loan. These assets aren’t similar to traditional collateral. Usually, collateral is tangible, like a house or car. However, these securities aren’t directly linked to the loan.

Collateral serves as a safety net for lenders. It guarantees that when a borrower can’t repay their loan, the lender will have something to fall back on.

Lenders make back the difference with collateral by selling it. For example, if a house is put up as collateral for a mortgage, the bank will sell it, sometimes for less than market value, to cover the lost money they incurred.

Most loans don’t require collateral, and even fewer want indirect security from a borrower. So, indirect security is usually a weaker type of collateral compared to traditional assets. However, there are cases where this type of backing is preferred.

Indirect Security is also a term for stocks. Indirect stocks give investors less decision-making and value than direct stocks.

Even though the term is the same, its meanings are completely different! So make sure to distinguish all of the meanings!

Key Takeaways

- Indirect security refers to a security interest in assets that are not directly held by the borrower but are instead held by a third party, such as a subsidiary or affiliate.

- Indirect securities are a type of security that is often used in complex financial transactions to provide additional protection for lenders.

- Indirect security is used to enhance the creditworthiness of a borrower by providing additional assurance to lenders.

- It can help mitigate risks and increase the likelihood of loan approval, especially in cases where the borrower's direct assets are insufficient or not readily available as collateral.

Types of Indirect Security

There are two main types of indirect security regarding loans. Both types can be used as collateral/banking. These securities are promises from another party besides the borrower and lender.

Guarantee

A guarantee is a promise from another party to take the financial responsibility of a borrower if they can’t pay their debt. Suppose the borrower does fail to pay back their loan. The guarantor (the other party) will repay the lender a portion or all of the debt.

Borrowers with low credit scores often need help securing loans. Their low score shows that the borrower needs help repaying debts and is not financially secure. Banks rarely lend to these individuals as they pose a large risk to the bank.

A guarantor can help alleviate this problem. A guarantor can secure a loan by promising the bank to pay back a loan if the borrower defaults. A guarantor's presence helps persuade banks to give loans to riskier borrowers.

Guarantors can take the form of multiple things. For example, guarantors can be family members, companies, or groups. But generally, companies are guarantors as single or small groups don’t have the needed capital to start paying back a loan suddenly.

For example, a Company, XYZ, wants to take out a loan, but the bank they applied to refuses their application, reasoning that the company doesn’t have the necessary collateral or some underlying reason.

Company XYZ then asks company ABC (A larger and more well-known company) to be their guarantor. Company ABC pledges to pay back XYZ’s loan if they default. The bank then gives the loan to XYZ as their position is much more stable now.

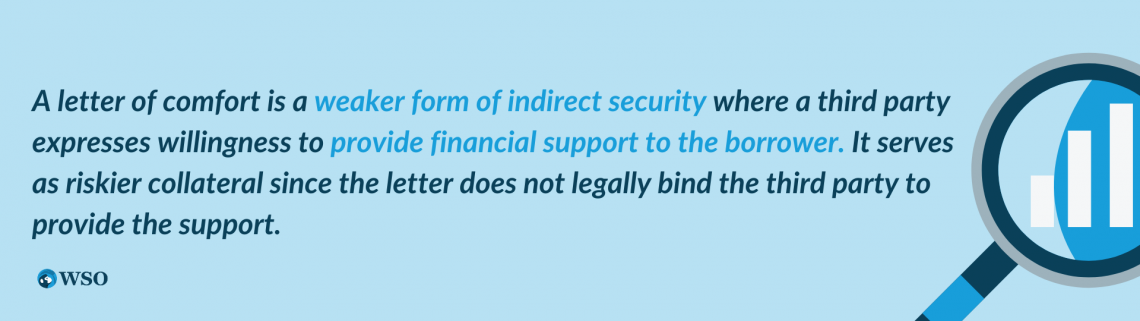

Letter of Comfort

Letter of Comfort is considered a weaker form of indirect security. The letter dictates that a third party is “willing” to provide financial support to the borrower. It usually is given by a parent company to its lower facilities. It is a document issued by a third party.

While letters of comfort can be used as collateral, they are letters that only dictate that a third party “wants to” support the borrower. The letter does not require them to. Although it is a riskier piece of collateral, most large companies wouldn’t risk their reputation by not paying off a loan.

Another form of a letter of comfort is a bank comfort letter (BCL). Banks may also issue these letters to a supplier. The letter states that the bank believes that the borrower is financially capable of paying off the loan.

But the letter simply says that the borrower is financially able to pay off a loan. It doesn’t dictate whether the bank will pay off any debt not paid for by the borrower.

For example, Borrower A wants to get a loan. But, unfortunately, their credit score is below average. So, to get a loan, they go to a large third-party source to get it to write them a letter of comfort.

The letter dictates that the third party affirms that they can help the borrower financially. The letter doesn’t dictate how much the party will give, in what form, or when. The letter simply intends that the third party wishes to help the borrower.

The borrower takes the letter and hands it to the bank, hoping it will accept it as backing. However, the bank sees the third party and, due to the size of the third party, accepts the letter as collateral and gives the borrower the loan.

If a borrower is incapable of securing a letter of comfort for any reason, this could indicate financial irresponsibility. The bank usually denies the application for a loan.

Banks usually only accept those who can get backing, especially those with a good track record.

Why are indirect securities weaker?

Indirect security is generally weaker than any form of collateral available. It isn’t a tangible asset that can be sold. It comes with a level of risk that the bank cannot account for, which creates uncertainty for the bank and a lower chance of securing a loan.

Both forms of indirect security affirm that someone else will pay the debt if the borrower defaults on their loans. However, the letter says little about how much or how the third party will pay off the loan.

This insecurity of payments is often not accepted by banks. Banks would like to see a tangible form of backing like traditional collateral. Unfortunately, letters don’t always secure a bank’s profits, let alone their lent-out credit, compared to assets that have value and can be sold quickly for a profit.

Compared to traditional assets, it is easy to see why banks are hesitant to accept these securities. To secure a loan, seeking more tangible collateral is best. A piece of indirect security isn’t likely to secure a loan.

Indirect Security with Stocks

Stock can be categorized into two sectors. Direct and indirect. Investors are given an option on which to buy and own.

Direct Stocks

Direct stocks are the most common. Whenever you buy a stock through a brokerage, through a trust, or with a partnership, you are buying direct stocks. As a result, you own these stocks, and you also get shareholder rights.

These shareholder rights allow you, a shareholder, to vote on what a company is to do and how it should be run. These stocks give investors power within a company but also make them liable for any stock price drops or poor company decisions.

Indirect Stocks

These are different from direct stocks. When you purchase stock through a mutual fund or exchange-traded funds, you don't own the stocks. When purchasing a mutual fund, the fund owns and operates the stocks. The fund simply holds the stocks on behalf of the investors.

You lose shareholder rights and liability because you don’t directly own the stocks. But, again, this is due to the mutual fund making the decisions.

When multiple investors buy a mutual fund, the mutual fund now has to represent the interests of the investors when deciding about a company.

These indirect securities include the Fidelity Growth & Income Portfolio (FGRIX) mutual fund or the Vanguard Equity Income Fund (VEIPX). Both these mutual funds hold securities, but the investor only earns money when the stock appreciates but doesn’t own shareholder privileges.

Why use indirect securities?

Although these securities are generally weaker than most collateral or real assets, they have their uses. For example, adding to a great portfolio could boost the chances of a bank accepting you as a borrower and giving you a loan.

1. Loans

Most banks can’t be won over with a single piece of security. Since indirect security is weaker than most securities/collateral, they aren’t used as collateral when applying for a loan.

In most instances, a borrower will have a third party give them a guarantee or letter of comfort to add on top of a good credit score and financial history. The extra layer of security, a piece of indirect security, can help secure a loan.

If you need to secure a loan and are afraid that your credit score isn’t good enough, a letter of comfort or a guarantee from a family member may be a good option. If they have a history of good credit and are financially stable, their backing can help persuade a bank.

2. Stocks

Although some investors, especially knowledge investors, prefer direct securities, average or inexperienced investors usually begin with investments in mutual funds.

These funds monitor and select which stocks to buy and sell. It becomes the fund's job to maintain the mutual fund's profitability and ensure the investor turns a profit. This management frees up the investor's time and allows them to make passive income without worrying about losing money in the stock market.

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?