Floating Charge

One type of security interest charge that permits a lender to claim a broader set of the company's assets, including the variable assets over time.

What Is a Floating Charge?

A floating charge is one type of security interest charge that permits a lender to claim a broader set of the company's assets, including the variable assets over time.

A floating charge is a charge over all the variable assets owned by a company or limited liability partnership as security for indebtedness.

Companies use these charges to secure loans and maintain asset flexibility. Floating charges are popular as a security device for two principal reasons:

-

From the lender’s perspective, the security will cover all the company's assets.

-

From the company’s perspective, although all of its assets are restricted because the security "floats", they are free to deal with the assets and use them in daily business operations, obtaining the maximum benefit from the lender.

Companies can use floating charges for securing a loan against an asset class instead of a single asset. Generally, a loan is secured by fixed assets such as plants, property, and equipment (PP&E).

With a floating charge, the underlying assets are variable short-term assets, such as inventory, accounts receivable, marketable securities, etc.

They let businesses buy/sell stocks and inputs without affecting their daily operations. By using their inventories as collateral, businesses can acquire loans and obtain funding.

Key Takeaways

- A floating charge is a type of security interest granted by a company to a lender over its current and future assets.

- This means the lender has a claim on the company's assets as security for a loan, but the specific assets aren't identified initially.

- A floating charge allows the company more flexibility in its day-to-day operations. The company can freely sell or dispose of assets as long as it remains a going concern (operational business).

- For a floating charge to be valid, it typically needs to be registered with the Companies House in the UK (or a relevant authority, depending on the location).

Fixed Charge vs. Floating Charge

A floating charge lets companies finance their operations while still using current assets such as inventory. However, if a company fails to repay the loan behind the charge, the charge crystallizes.

A fixed charge is a crystallized floating charge. Crystallization occurs if a company fails to repay the loan or enters liquidation, but it can also happen if a company ends its operations or if the lender enters a court to appoint a receiver.

A fixed charge is a loan or mortgage secured on tangible assets, such as land, buildings, ships, machinery, shares, and intellectual property (copyright, trademarks, patents, etc.).

A fixed charge is generally attached to a set number of assets, but a floating charge is attached to ever-changing assets.

Since fixed charges are overhead costs that are not closely associated with activity levels, a business will likely incur these costs even if production is greatly reduced.

For instance, if an oil company can be expected to have a much higher proportion of fixed charges than a consulting practice, it is much easier for the oil refinery to predict its future expenses. When expenses are largely made of fixed charges, it is much easier for a business to predict those costs through a budget, since these fixed costs rarely change.

Floating Charge Example

Let's take an example to help understand better.

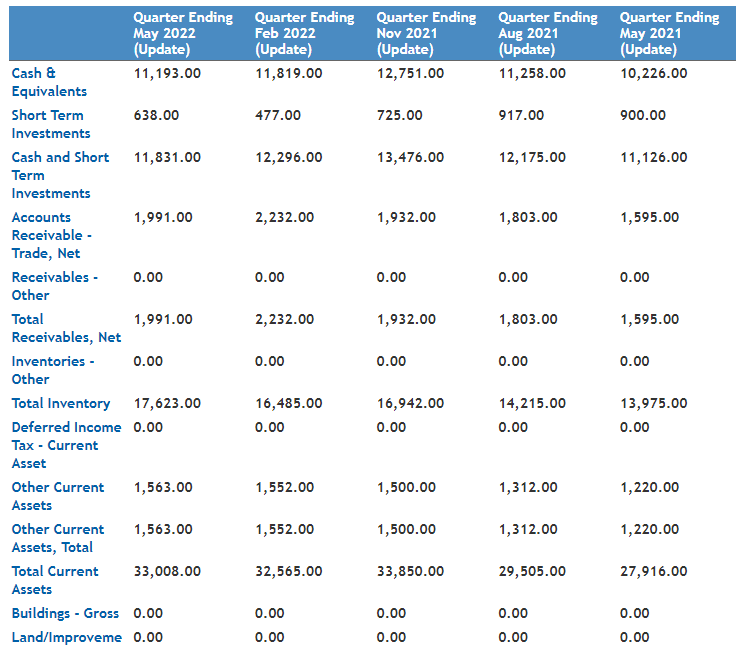

Costco Wholesale Corporation is one of the largest wholesale retailers in the nation. As of 2016, it was the world’s largest retailer of beef, rotisserie chicken, organic foods, and wine.

Let’s say the company entered a loan with a large bank and decided to use its inventory as collateral. The lender can either exercise his control over the inventory or enter a floating charge, whichever the loan agreement specifies.

We can observe here that the value of inventory varies from one quarter to another. For example, the inventory value was $17.623B for the quarter ending May 31, 2022, while it was $16.485B for the previous quarter ending February 28, 2022.

Therefore, we can infer that the asset used to secure a loan, inventory in our case, is allowed to vary in quantity and price.

Thus, a floating charge allows companies to use current assets to finance business operations and tasks.

If a company cannot make the promised repayments, enters liquidation, or faces financial difficulties, the charge will crystallize into a fixed charge. In addition, it means that the company is now not allowed to dispose of any underlying asset under the loan.

Floating Charge Advantages and Disadvantages

The charge allows unrestricted use of the asset held as security. It is a solid cover against all the business assets and still allows daily operations to occur.

An unusual thing about floating and fixed charges is that at least one will give priority to another charge if liquidation occurs. If the priority is not stated, then the charge created before will be given priority.

Advantages are:

- The advantage of a floating charge is that before insolvency, it allows the charged assets to be bought and sold during the course of a firm’s life without reference to the lender.

- As the value of the assets changes, the value of the charge also changes. It does not apply to specific assets, it applies to all assets for a given period of time.

Disadvantages are:

- They may be invalid if created within a certain period prior to a company's insolvency. The relevant period depends on whether the charge is in favor of an unconnected or a connected person.

Researched and authorized by Madhav Badithela | Linkedin

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?