Acquisition and Payment Cycle

A business process that includes sequential steps that encompass the acquisition of goods and services and making payments to vendors.

What is the Acquisition and Payment Cycle?

The Acquistion and Payment Cylce, or PPP Cycle for Purchases, Payables, and Payments, is a business process that includes sequential steps that encompass the acquisition of goods and services and making payments to vendors.

The acquisition and payment cycle primarily consists of two groups of transactions: the acquisition class and the cash disbursements.

For the acquisition class, the typical journal entry is a debit to inventory or a cost and a credit to accounts payable. The classification assertion is crucial given that numerous alternative debits could complete the journal entry.

On the other hand, cash disbursements are the second class of purchase and payment cycle transactions. The journal entry for this class is only a debit to accounts payable and a cash credit. Overall, this cycle focuses on accrued payables and clearing them with cash.

Even though many businesses have unique internal procedures and employ electronic-based techniques, a purchase request created by a firm employee often initiates the procedure.

For example, a buy request is a document that specifies the items and the quantity needed. The purchasing division receives the document and creates a purchase order.

Employees often have access only to a list of approved vendors. Once the subsequent department has received the ordered goods, the business issues a receiving report.

The report is delivered to the accounting department's accounts payable team, which should agree with the purchase order.

Here, the employee compares the vendor's invoice to the products received before recording the journal entry for accounts payable. The money is then really disbursed when the Treasury processes the payment.

Key Takeaways

- The acquisition and payment cycle, also known as the purchasing cycle, encompasses all activities related to the procurement of goods and services and the subsequent payment for those goods and services.

- The accounting procedure auditors use to analyze a corporation's financial statements and supporting documents is an audit cycle.

- Five appropriate assertions for the class of transactions are cut-off, classification, completeness, occurrence, and accuracy.

- The purchase and payment cycle of a business is prone to error. Companies can exaggerate the worth of the inventory they buy, which gives the impression that assets are larger than they are.

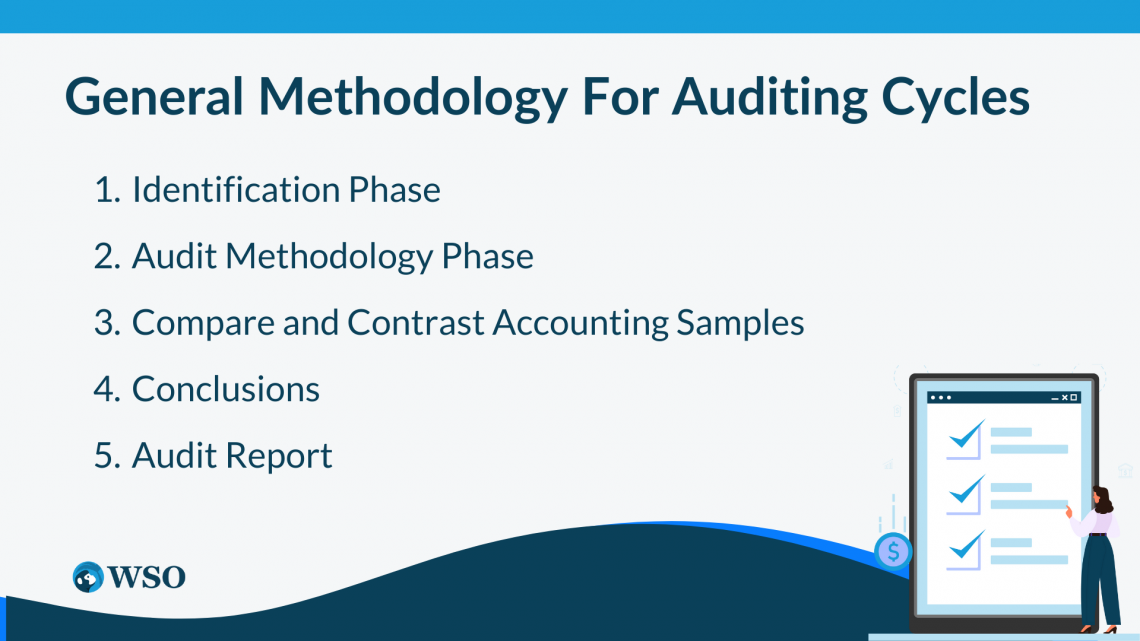

General Methodology for Auditing Cycles

The accounting procedure auditors use to analyze a corporation's financial statements and supporting documents is an audit cycle.

An audit cycle refers to the procedures an auditor follows to confirm the accuracy of the company's financial data. Depending on the audit cycle, different tasks may need to be completed at different times.

For instance, inventory counts may be due in October, while account receivables determinations may be due in November. When auditing cycles for various businesses, the usual method is to:

1. Identification Phase

The identification phase is the first step, during which the company meets with auditors to determine which accounting areas require further study.

2. Audit Methodology Phase

During this stage, the auditors determine the methodology and approach for gathering and analyzing the data.

3. Compare and Contrast Accounting Samples

The audit fieldwork stage involves the examination and comparison of accounting samples. Auditors select a representative sample of transactions or documents related to the audited cycle.

NOTE

Auditors assess the reliability and accuracy of these samples, comparing them to established standards and policies.

4. Conclusions

In the fourth stage, the management review meeting, the auditors present their conclusions to the company's management team.

They communicate the findings, including any discrepancies or areas of concern identified during the audit, and provide an opportunity to clarify the audit results.

5. Audit Report

In the final phase, the audit report is prepared and delivered to management. This report comprehensively overviews the audit process, findings, and recommendations.

It highlights any inconsistencies or deficiencies discovered in the company's financial accounts, aiming to enhance transparency and accountability.

Important Internal Controls For Acquisitions and Disbursements

Several internal controls can be implemented to ensure the effectiveness and accuracy of the acquisition and payment cycles. Here are some key controls for each of the five appropriate assertions:

1. Occurrence Assertion

The events and transactions that have been noted or revealed have taken place and are relevant to the entity.

According to internal controls relating to the occurrence assertion, each purchase is supported by the required supporting papers, such as the buy request, purchase order, receipt of the report, and vendor's invoice.

2. Completeness Assertion

All transactions and events that needed to be reported have been reported, and the financial statements now contain all necessary associated disclosures.

NOTE

Some controls related to the classification assumption include getting sufficient supervisor clearance for journal entries, having a good list or chart of accounts with descriptions of each, and comparing balances to budgeted amounts.

3. Classification Assertion

The appropriate accounts have been used to record transactions and events.

4. Cut-off Assertion

Events and transactions have been documented during the appropriate accounting period.

5. Accuracy Assertion

Amounts and other information pertaining to the transactions and events have been properly recorded, and the relevant disclosures have been measured and explained.

NOTE

A purchase cannot "occur" without these papers. Hence it should not have been registered.

Other controls include:

- Having higher-level employees approve purchase orders.

- Canceling paperwork after a transaction has been documented or accounted for.

- Approving any modifications to the vendor list.

Purchase orders and receiving reports are often pre-numbered and accounted for regarding the completeness assertion. Therefore, it will be simple to identify the issue if a number has been registered twice or is absent from the list.

The Auditor's Role

An auditor plays a crucial role in ensuring a company's financial records' accuracy, compliance, and integrity. Here are the key responsibilities and functions of an auditor:

Verification of Compliance

Integrating compliance into internal processes is a realistic way to comply with compliance obligations. Compliance regulations must be adhered to as closely as feasible. Compliance verifications take several forms.

You may be able to meet the requirements set in their specific industries with the aid of these verifications.

Evaluation of Internal Controls

With a thorough grasp of controls, an auditor may see risks related to the client's internal controls and, as a result, may plan and implement the necessary countermeasures.

NOTE

A lack of understanding of controls prevents the auditor from having a solid foundation to assess the risks of material misstatement, which should be related to the audit methods.

Examination of Financial Records

Through different documented transactions, financial statements depict a company's funding, investing, and operating operations. The financial statements were created domestically, so it is possible they were prepared fraudulently.

Questioning and Inquiry

A simple inquiry testing technique uses interview-style questions with the point of contact for some controls. It is considered a weaker kind of evidence since the accuracy and sincerity of the interviewee determine the quality of the information obtained through inquiry.

NOTE

Auditors enquire about managers, accountants, and other key personnel using the inquiry method to obtain some pertinent information.

Risk Assessment and Recommendations

A risk assessment is a methodical procedure carried out by a qualified individual that entails locating, evaluating, and controlling any risks or dangers present in a circumstance or location.

This decision-making tool tries to identify which actions should be taken to mitigate or control such risks and to indicate which should be prioritized based on their likelihood and potential effects on the company.

How to Audit the Acquisition and Payment Cycle

A business's purchase and payment cycle is prone to error. Companies can exaggerate the worth of the inventory they buy, giving the impression that assets are larger than they actually are.

Management may overlook or undervalue accounts payable, exaggerating financial strength. To avoid this situation, management and auditors monitor internal controls and important acquisition accounts closely.

Assess Risks

Depending on the environment, a firm may face distinct dangers at different stages of the acquisition cycle. Companies that sell low-margin items in a highly competitive market are incentivized to manipulate their margins through inventory and COGS valuation.

Without excellent accounting department staff with operational knowledge, businesses might not adequately track purchase and cash disbursement paperwork.

Depending on the organization's intrinsic strengths and weaknesses, auditors will pay closer attention to personalized risk factors and identify areas where there may be a higher risk of misstatement or manipulation.

Ensure Controls are in Place

The likelihood of fraud or errors in the company's purchasing system decreases with greater internal controls in place.

The best businesses mandate that their purchasing representatives only work with recognized vendors and conduct frequent vendor reviews. As a result, there is a lower possibility of fraud and kickbacks.

NOTE

The separation of roles and requirements for approval in the purchasing and cash disbursement processes will be examined by auditors. These measures help organizations catch honest mistakes and deter employees from trying to steal money.

Evaluate Inventory and COGS

Auditors want to ensure inventory isn't exaggerated because it's a big asset. Auditors will see the physical inventory count to check that the numbers add up and conduct their sample count.

They will verify inventory purchase transactions close to a financial cutoff period to ensure that they are recorded appropriately.

NOTE

Older inventory that the business hasn't been able to sell will receive special attention from them because there's a good likelihood that its worth may have decreased over time.

Look at Accounts Payable and Related Expenses

Auditors will look for unrecorded accounts payable because they account for a sizable portion of the company's debts to third parties.

The main ledger, which decides the financial statements, frequently takes transactions from a subsidiary accounts payable ledger to verify that they are also recorded. They might contact important suppliers and vendors to see if they concur with the amount the business claims to owe them.

NOTE

Auditors will test transactions to check if inventory values agree with the vendor's sales price because purchasing influences inventory value.

Analyze Vendor Relationships

You probably can't run your entire business in-house, whether a Fortune 100 firm or a mom-and-pop shop.

At this point, the vendors step in. Vendors may offer services (coaching, photography, social media creation) or items (fresh fruit, hardware, car fleets) that can be essential to your company's success.

How to Simplify the Acquisition and Payment Cycle

As the world becomes increasingly digital, how businesses function, exchange commodities for cash, and pay for services has changed.

Many business processes are still needlessly complex—and in some cases, redundant — even though they have been reduced in almost every department over the years. It is a lengthy procedure that involves many people, departments, and outside organizations.

NOTE

It involves each step, from finding a supplier to completing a payment once the services or commodities are obtained.

To simplify the acquisition and payment cycle, businesses can adopt certain strategies and leverage digital advancements. Here are some:

1. Embrace Technology

The rise of artificial intelligence (AI), the Internet of Things (IoT), and other digital advancements have altered how organizations conduct contracts, purchase orders, invoices, and more.

This also impacts the entire procurement and payment cycle; a corporation must determine what it needs to purchase.

2. Organizational Change and Culture

Companies will probably need to make organizational and cultural modifications when switching to an automated strategy.

While some businesses may be happy with their current business practices, others will find a way to streamline their acquisition and payment procedures by implementing or embracing new technologies.

3. Establish a Single Point of Contact

Streamlining your procurement department is crucial in improving your sales and procurement procedures. A single point of contact (SPOC), a central procurement contact, can help.

NOTE

A SPOC makes sure that everyone involved knows where to turn if they need to make a purchase.

4. Automate the Invoice Matching Process

Paying your provider is the next step after acquiring goods or services. However, many businesses still use manual invoice matching procedures, which might hinder development needlessly.

NOTE

By comparing the data from a supplier with the data within your business, automated solutions can assist in speeding up the process.

5. Change the Way You Manage Contracts

Businesses frequently strike a balance between having too little and too much paperwork while maintaining important contracts.

As a result, there are sometimes several redundant tasks to complete. Such tasks include filling out the same paperwork multiple times in different locations.

Using AI, you can design contracts that adjust to each unique business environment, saving time on repetitive activities. Another method for streamlining the contract administration procedure is to use managed service providers (MSPs).

Free Resources

To continue learning and advancing your career, check out these additional helpful WSO resources:

or Want to Sign up with your social account?